Adobe - Future of Creativity Study

Global Study | 2022 | 51 pages

CREATORS IN THE CREATOR ECONOMY A GLOBAL STUDY

ADOBE CREATORS IN THE CREATOR ECONOMY INTRODUCTION TABLE OF CONTENTS STUDY OVERVIEW 3 EXECUTIVE SUMMARY 7 CREATIVE HOT SPOTS AND MARKET 13 DIFFERENCES AT A GLANCE THE CURRENT STATE OF CREATORS 23 CREATING ON SOCIAL IS ESSENTIAL 33 FOR EMOTIONAL WELL-BEING A CALL FOR SOCIAL CAUSE CREATORS 40 2

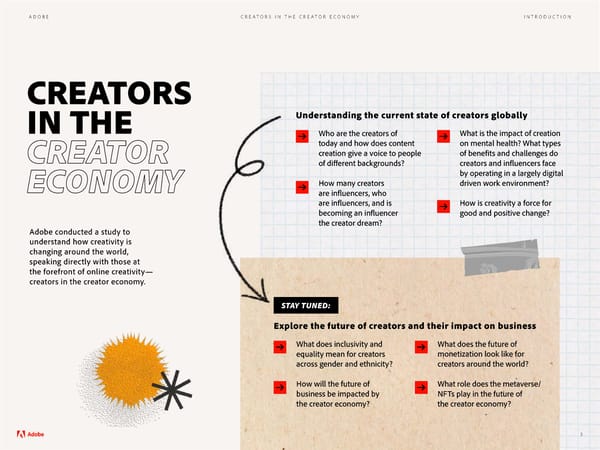

ADOBE CREATORS IN THE CREATOR ECONOMY INTRODUCTION CREATORS IN THE Understanding the current state of creators globally Who are the creators of What is the impact of creation today and how does content on mental health? What types CREATOR creation give a voice to people of bene昀椀ts and challenges do of di昀昀erent backgrounds? creators and in昀氀uencers face by operating in a largely digital ECONOMY How many creators driven work environment? are in昀氀uencers, who are in昀氀uencers, and is How is creativity a force for becoming an in昀氀uencer good and positive change? the creator dream? Adobe conducted a study to understand how creativity is changing around the world, speaking directly with those at the forefront of online creativity— creators in the creator economy. STAY TUNED: Explore the future of creators and their impact on business What does inclusivity and What does the future of equality mean for creators monetization look like for across gender and ethnicity? creators around the world? How will the future of What role does the metaverse/ business be impacted by NFTs play in the future of the creator economy? the creator economy? 3

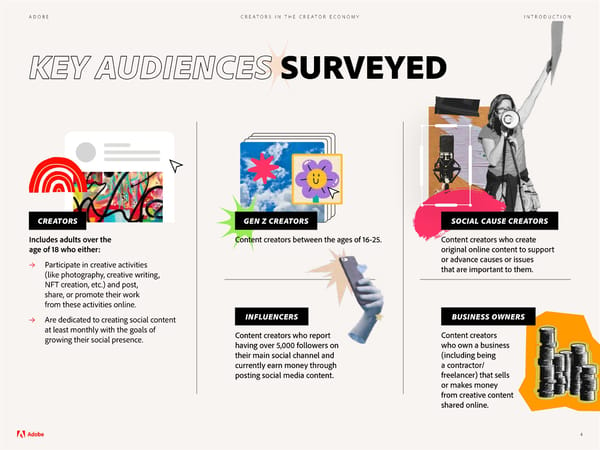

ADOBE CREATORS IN THE CREATOR ECONOMY INTRODUCTION KEY AUDIENCES SURVEYED CREATORS GEN Z CREATORS SOCIAL CAUSE CREATORS Includes adults over the Content creators between the ages of 16-25. Content creators who create age of 18 who either: original online content to support → Participate in creative activities or advance causes or issues (like photography, creative writing, that are important to them. NFT creation, etc.) and post, share, or promote their work from these activities online. → Are dedicated to creating social content INFLUENCERS BUSINESS OWNERS at least monthly with the goals of Content creators who report Content creators growing their social presence. having over 5,000 followers on who own a business their main social channel and (including being currently earn money through a contractor/ posting social media content. freelancer) that sells or makes money from creative content shared online. 4

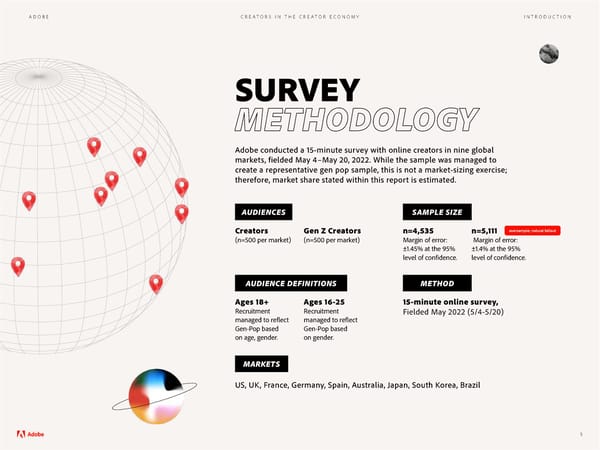

ADOBE CREATORS IN THE CREATOR ECONOMY INTRODUCTION SURVEY METHODOLOGY Adobe conducted a 15-minute survey with online creators in nine global markets, fielded May 4–May 20, 2022. While the sample was managed to create a representative gen pop sample, this is not a market-sizing exercise; therefore, market share stated within this report is estimated. AUDIENCES SAMPLE SIZE Creators Gen Z Creators n=4,535 n=5,111 oversample; natural fallout (n=500 per market) (n=500 per market) Margin of error: Margin of error: ±1.45% at the 95% ±1.4% at the 95% level of con昀椀dence. level of con昀椀dence. AUDIENCE DEFINITIONS METHOD Ages 18+ Ages 16-25 15-minute online survey, Recruitment Recruitment Fielded May 2022 (5/4-5/20) managed to re昀氀ect managed to re昀氀ect Gen-Pop based Gen-Pop based on age, gender. on gender. MARKETS US, UK, France, Germany, Spain, Australia, Japan, South Korea, Brazil 5

ADOBE CREATORS IN THE CREATOR ECONOMY EXECUTIVE SUMMARY EXECUTIVE SUMMARY EXECUTIVE SUMMARY SUMMARYEXECUTIVE SUMMARY EXECUTIVE SUMMARYEXECUTIVE SUMMARY EXECUTIVE SUMMARY 6 EXECUTIVE SUMMARY

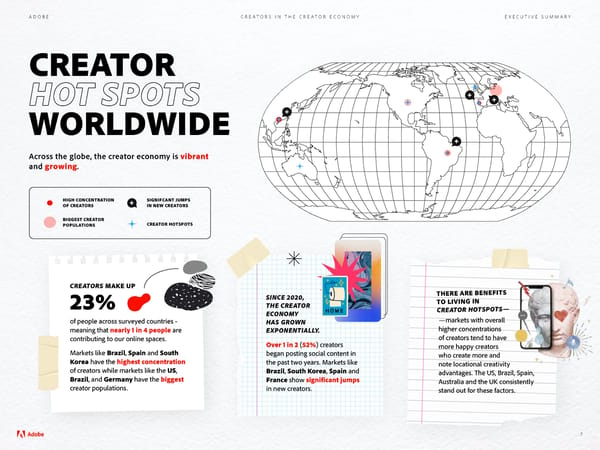

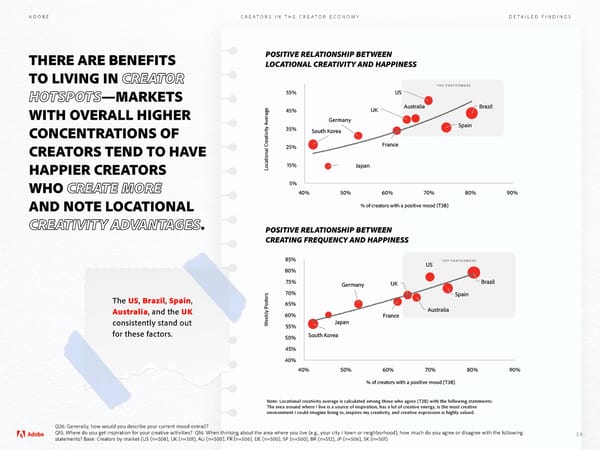

ADOBE CREATORS IN THE CREATOR ECONOMY EXECUTIVE SUMMARY CREATOR HOT SPOTS WORLDWIDE Across the globe, the creator economy is vibrant and growing. HIGH CONCENTRATION SIGNIFCANT JUMPS OF CREATORS IN NEW CREATORS BIGGEST CREATOR POPULATIONS CREATOR HOTSPOTS CREATORS MAKE UP ENEFITS E B E AR SINCE 2020, THER G IN IVIN 23% THE CREATOR TO L TS— TSPO TOR HO EA ECONOMY CR of people across surveyed countries - HAS GROWN —markets with overall meaning that nearly 1 in 4 people are EXPONENTIALLY. higher concentrations contributing to our online spaces. of creators tend to have Over 1 in 2 (52%) creators more happy creators Markets like Brazil, Spain and South began posting social content in who create more and Korea have the highest concentration the past two years. Markets like note locational creativity of creators while markets like the US, Brazil, South Korea, Spain and advantages. 吀栀e US, Brazil, Spain, Brazil, and Germany have the biggest France show signi昀椀cant jumps Australia and the UK consistently creator populations. in new creators. stand out for these factors. 7

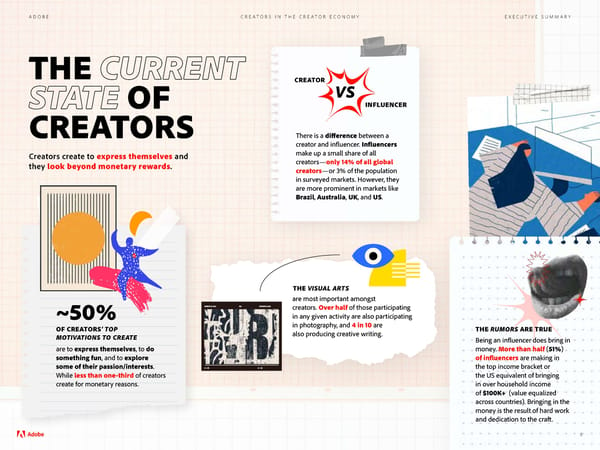

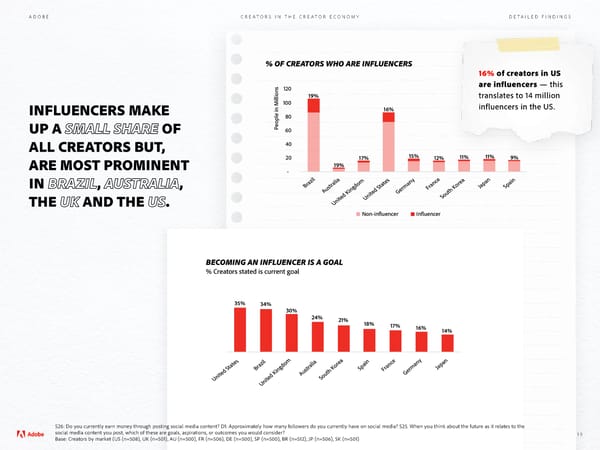

ADOBE CREATORS IN THE CREATOR ECONOMY EXECUTIVE SUMMARY THE CURRENT CREATOR VS STATE OF INFLUENCER CREATORS 吀栀ere is a di昀昀erence between a creator and in昀氀uencer. In昀氀uencers Creators create to express themselves and make up a small share of all they look beyond monetary rewards. creators—only 14% of all global creators—or 3% of the population in surveyed markets. However, they are more prominent in markets like Brazil, Australia, UK, and US. THE VISUAL ARTS are most important amongst creators. Over half of those participating ~50% in any given activity are also participating OF CREATORS’ TOP in photography, and 4 in 10 are THE RUMORS ARE TRUE MOTIVATIONS TO CREATE also producing creative writing. Being an in昀氀uencer does bring in are to express themselves, to do money. More than half (51%) something fun, and to explore of in昀氀uencers are making in some of their passion/interests. the top income bracket or While less than one-third of creators the US equivalent of bringing create for monetary reasons. in over household income of $100K+ (value equalized across countries). Bringing in the money is the result of hard work and dedication to the cra昀琀. 8

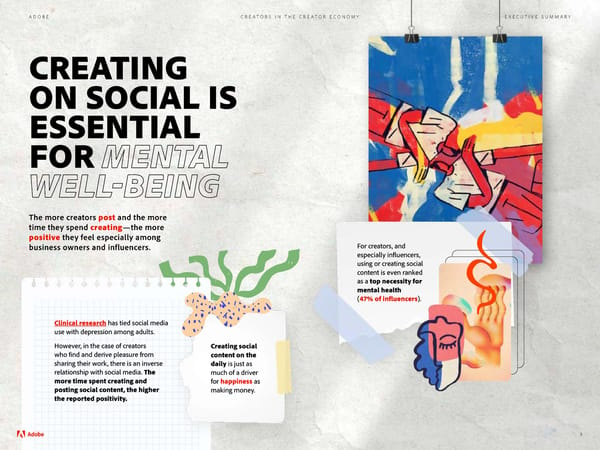

ADOBE CREATORS IN THE CREATOR ECONOMY EXECUTIVE SUMMARY CREATING ON SOCIAL IS ESSENTIAL MENTAL FOR WELL-BEING The more creators post and the more time they spend creating—the more positive they feel especially among business owners and influencers. For creators, and especially in昀氀uencers, using or creating social content is even ranked as a top necessity for mental health (47% of in昀氀uencers). Clinical research has tied social media use with depression among adults. However, in the case of creators Creating social who 昀椀nd and derive pleasure from content on the sharing their work, there is an inverse daily is just as relationship with social media. 吀栀e much of a driver more time spent creating and for happiness as posting social content, the higher making money. the reported positivity. 9

ADOBE CREATORS IN THE CREATOR ECONOMY EXECUTIVE SUMMARY A CALL FOR SOCIAL CAUSE CREATORS Creators agree that creating online content Creators are the first to say that supporting has a big impact on advancing causes— social causes is important and that especially in昀氀uencers (74%) and social cause creating online content has a big impact creators (73%). on advancing causes. However, only 1 in 4 creators use their content creation abilities to create original social cause content. 吀栀ere are large bene昀椀ts to creating social cause content— social cause creators feel the most positive and are For those fearing an impact on more likely to create more monetization, many social cause o昀琀en in the future. creators earn money from social despite posting potentially sensitive content. Similarly, in昀氀uencers don’t shy away from social cause activism—in fact, they embrace it. 10

ADOBE CREATORS IN THE CREATOR ECONOMY INTRODUCTION DETAILED FINDINGS DETAILED FINDINGS DETAILED FINDINGSDETAILED FINDINGS DETAILED FINDINGSDETAILED FINDINGS DETAILED FINDINGS 11 DETAILED FINDINGS

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS CREATIVE HOT SPOTS AND MARKET DIFFERENCES AT A GLANCE 12

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS A CREATIVE PERSON... “ Sees, imagines and creates with everything that surrounds it.” — CREATOR, SPAIN 13

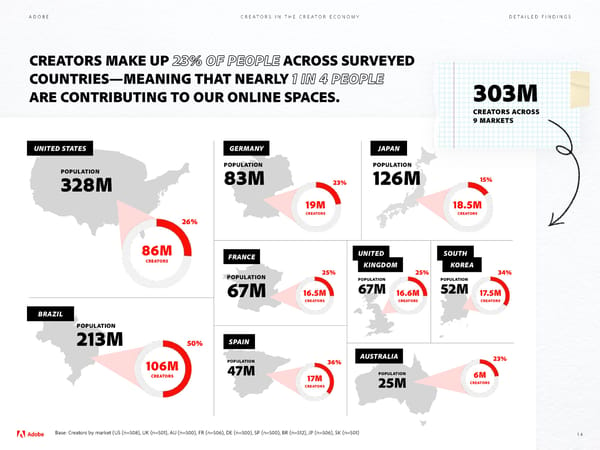

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS CREATORS MAKE UP 23% OF PEOPLE ACROSS SURVEYED COUNTRIES—MEANING THAT NEARLY 1 IN 4 PEOPLE 303M ARE CONTRIBUTING TO OUR ONLINE SPACES. CREATORS ACROSS 9 MARKETS UNITED STATES GERMANY JAPAN POPULATION POPULATION POPULATION 328M 83M 23% 126M 15% 19M 18.5M CREATORS CREATORS 26% 86M FRANCE UNITED SOUTH CREATORS KINGDOM KOREA POPULATION 25% 25% 34% POPULATION POPULATION 67M 16.5M 67M 16.6M 52M 17.5M CREATORS CREATORS CREATORS BRAZIL POPULATION 213M 50% SPAIN AUSTRALIA 23% 106M POPULATION 36% CREATORS 47M 17M POPULATION 6M CREATORS 25M CREATORS Base: Creators by market (US (n=508), UK (n=501), AU (n=500), FR (n=506), DE (n=500), SP (n=500), BR (n=512), JP (n=506), SK (n=501) 14

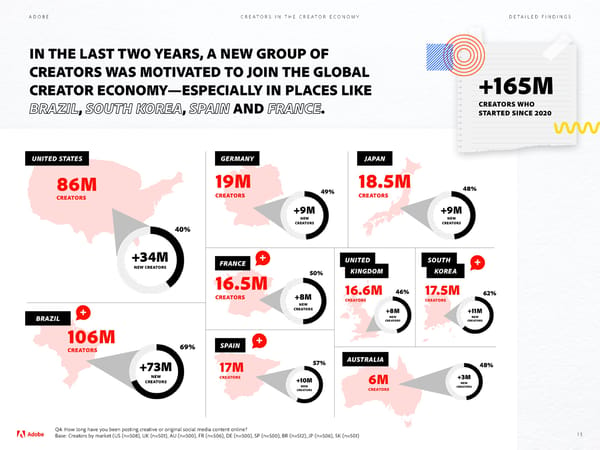

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS IN THE LAST TWO YEARS, A NEW GROUP OF CREATORS WAS MOTIVATED TO JOIN THE GLOBAL +165M CREATOR ECONOMY—ESPECIALLY IN PLACES LIKE BRAZIL, SOUTH KOREA, SPAIN AND FRANCE. CREATORS WHO STARTED SINCE 2020 UNITED STATES GERMANY JAPAN 86M 19M 18.5M 48% CREATORS 49% CREATORS CREATORS +9M +9M NEW NEW CREATORS CREATORS 40% +34M FRANCE UNITED SOUTH NEW CREATORS KINGDOM KOREA 16.5M 50% CREATORS +8M 16.6M 46% 17.5M 62% CREATORS CREATORS NEW CREATORS +8M +11M BRAZIL NEW NEW CREATORS CREATORS 106M 69% SPAIN CREATORS +73M 17M 57% AUSTRALIA 48% NEW CREATORS +10M +3M CREATORS 6M NEW NEW CREATORS CREATORS CREATORS Q4: How long have you been posting creative or original social media content online? Base: Creators by market (US (n=508), UK (n=501), AU (n=500), FR (n=506), DE (n=500), SP (n=500), BR (n=512), JP (n=506), SK (n=501) 15

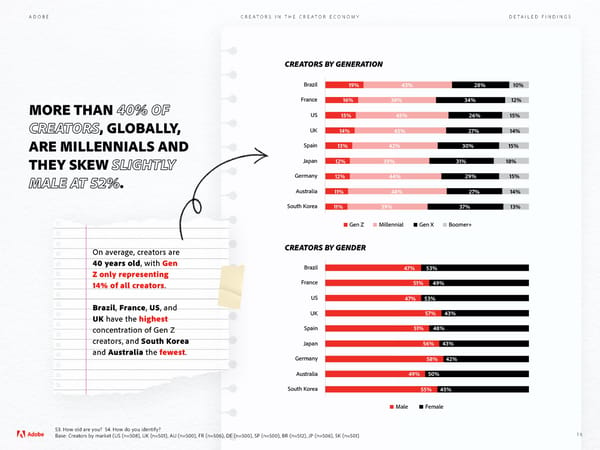

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS CREATORS BY GENERATION Brazil 19% 43% 28% 10% MORE THAN 40% OF France 16% 38% 34% 12% US 15% 45% 26% 15% CREATORS, GLOBALLY, UK 14% 45% 27% 14% ARE MILLENNIALS AND Spain 13% 42% 30% 15% THEY SKEW SLIGHTLY Japan 12% 39% 31% 18% MALE AT 52%. Germany 12% 44% 29% 15% Australia 11% 48% 27% 14% South Korea 11% 39% 37% 13% Gen Z Millennial Gen X Boomer+ On average, creators are CREATORS BY GENDER 40 years old, with Gen Brazil 47% 53% Z only representing 14% of all creators. France 51% 49% US 47% 53% Brazil, France, US, and UK 57% 43% UK have the highest concentration of Gen Z Spain 51% 48% creators, and South Korea Japan 56% 43% and Australia the fewest. Germany 58% 42% Australia 49% 50% South Korea 55% 45% Male Female S3S3. H. Hoow old arw old are ye youou? S4. H? S4. Hoow do yw do you ideou identntiiffyy?? BBasasee: C: Crreeaatortors bs by mary markkeet (t (US (US (n=508)n=508), U, UK (K (n=501)n=501), A, AU (U (n=500)n=500), FR (, FR (n=50n=506)6), DE (, DE (n=500)n=500), SP (, SP (n=500)n=500), BR (, BR (n=5n=5112)2), J, JP (P (n=50n=506)6), SK (, SK (n=501)n=501) 16

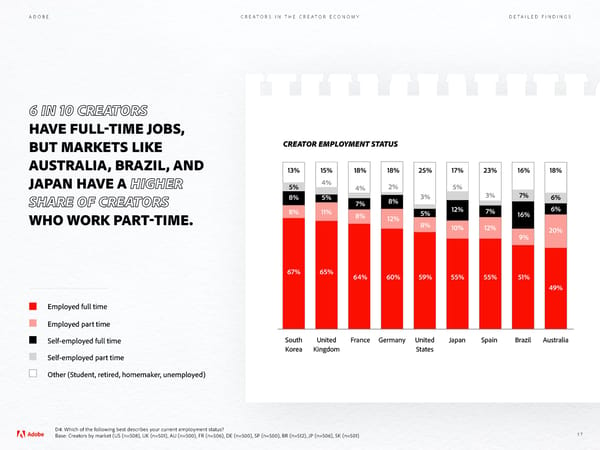

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS 6 IN 10 CREATORS HAVE FULL-TIME JOBS, BUT MARKETS LIKE CREATOR EMPLOYMENT STATUS AUSTRALIA, BRAZIL, AND 13% 15% 18% 18% 25% 17% 23% 16% 18% JAPAN HAVE A HIGHER 5% 4% 4% 2% 5% 8% 5% 8% 3% 3% 7% 6% SHARE OF CREATORS 7% 12% 6% 2% 8% 11% 8% 5% 7% 16% WHO WORK PART-TIME. 12% 8% 10% 12% 20% 9% 67% 65% 64% 60% 59% 55% 55% 51% 49% Employed full time Employed part time Self-employed full time South United France Germany United Japan Spain Brazil Australia Korea Kingdom States Self-employed part time Other (Student, retired, homemaker, unemployed) D4: Which of the following best describes your current employment status? Base: Creators by market (US (n=508), UK (n=501), AU (n=500), FR (n=506), DE (n=500), SP (n=500), BR (n=512), JP (n=506), SK (n=501) 17

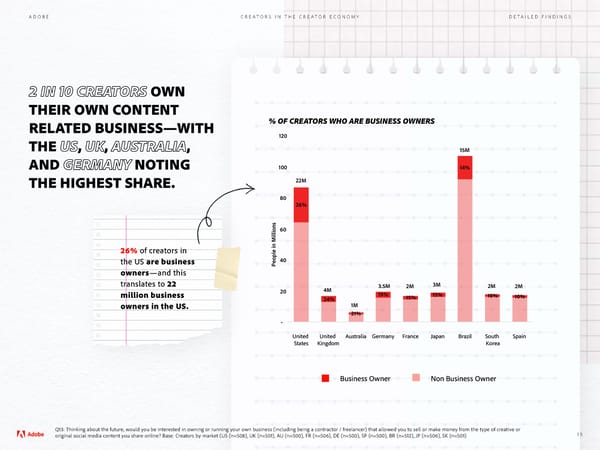

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS 2 IN 10 CREATORS OWN THEIR OWN CONTENT RELATED BUSINESS—WITH % OF CREATORS WHO ARE BUSINESS OWNERS THE US, UK, AUSTRALIA, 120 15M AND GERMANY NOTING 100 14% THE HIGHEST SHARE. 22M 80 26% 60 26% of creators in the US are business People in Millions 40 owners—and this translates to 22 3.5M 2M 3M 2M 2M 20 4M 19% 15% million business 24% 15% 10% 10% owners in the US . 1M 21% - United United Australia Germany France Japan Brazil South Spain States Kingdom Korea Business Owner Non Business Owner Q13: Thinking about the future, would you be interested in owning or running your own business (including being a contractor / freelancer) that allowed you to sell or make money from the type of creative or original social media content you share online? Base: Creators by market (US (n=508), UK (n=501), AU (n=500), FR (n=506), DE (n=500), SP (n=500), BR (n=512), JP (n=506), SK (n=501) 18

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS % OF CREATORS WHO ARE INFLUENCERS 16% of creators in US 120 are influencers — this 19% translates to 14 million 100 influencers in the US . INFLUENCERS MAKE 16% 80 UP A SMALL SHARE OF People in Millions 60 ALL CREATORS BUT, 40 20 17% 15% 12% 11% 11% 9% ARE MOST PROMINENT 19% - IN BRAZIL, AUSTRALIA, Brazil France Japan Spain Australia Germany United States South Korea THE UK AND THE US. United Kingdom Non-in uencer In uencer BECOMING AN INFLUENCER IS A GOAL % Creators stated is current goal 35% 34% 30% 24% 21% 18% 17% 16% 14% Brazil Spain France Japan Australia Germany United States South Korea United Kingdom S26: Do you currently earn money through posting social media content? D1: Approximately how many followers do you currently have on social media? S25. When you think about the future as it relates to the social media content you post, which of these are goals, aspirations, or outcomes you would consider? 19 Base: Creators by market (US (n=508), UK (n=501), AU (n=500), FR (n=506), DE (n=500), SP (n=500), BR (n=512), JP (n=506), SK (n=501)

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS THERE ARE BENEFITS POSITIVE RELATIONSHIP BETWEEN LOCATIONAL CREATIVITY AND HAPPINESS TO LIVING IN CREATOR TOP PERFORMERS HOTSPOTS—MARKETS 55% US WITH OVERALL HIGHER 45% UK Australia Brazil Germany Spain CONCENTRATIONS OF 35% South Korea CREATORS TEND TO HAVE 25% France HAPPIER CREATORS Locational Creativity Average15% Japan WHO CREATE MORE 5% 40% 50% 60% 70% 80% 90% % of creators with a positive mood (T3B) AND NOTE LOCATIONAL CREATIVITY ADVANTAGES. POSITIVE RELATIONSHIP BETWEEN CREATING FREQUENCY AND HAPPINESS 85% US TOP PERFORMERS 80% 75% Germany UK Brazil 70% Spain The US, Brazil, Spain, 65% Australia, and the UK 60% Australia France consistently stand out Weekly Posters55% Japan for these factors. 50% South Korea 45% 40% 40% 50% 60% 70% 80% 90% % of creators with a positive mood (T3B) Note: Locational creativity average is calculated among those who agree (T2B) with the following statements: The area around where I live is a source of inspiration, has a lot of creative energy, is the most creative environment I could imagine living in, inspires my creativity, and creative expression is highly valued. Q26: Generally, how would you describe your current mood overall? Q15. Where do you get inspiration for your creative activities? Q16. When thinking about the area where you live (e.g., your city / town or neighborhood), how much do you agree or disagree with the following 20 statements? Base: Creators by market (US (n=508), UK (n=501), AU (n=500), FR (n=506), DE (n=500), SP (n=500), BR (n=512), JP (n=506), SK (n=501)

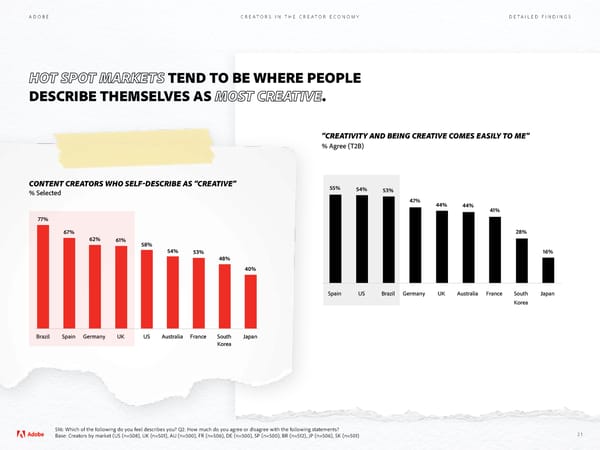

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS HOT SPOT MARKETS TEND TO BE WHERE PEOPLE DESCRIBE THEMSELVES AS MOST CREATIVE. “CREATIVITY AND BEING CREATIVE COMES EASILY TO ME” % Agree (T2B) CONTENT CREATORS WHO SELF-DESCRIBE AS “CREATIVE” 55% 54% % Selected 53% 47% 44% 44% 41% 77% 67% 28% 62% 61% 58% 54% 53% 16% 48% 40% Spain US Brazil Germany UK Australia France South Japan Korea Brazil Spain Germany UK US Australia France South Japan Korea S16: Which of the following do you feel describes you? Q2: How much do you agree or disagree with the following statements? Base: Creators by market (US (n=508), UK (n=501), AU (n=500), FR (n=506), DE (n=500), SP (n=500), BR (n=512), JP (n=506), SK (n=501) 21

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS THE CURRENT STATE OF CREATORS 22

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS A CREATIVE PERSON... “ Isn’t afraid of experimenting and expressing themselves.” — CREATOR, UNITED STATES 23

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS FREEDOM TO EXPRESS ONESELF IS THE NUMBER ONE MOTIVATOR FOR CREATORS. Other top motivators include wanting to do something fun and explore an interest or passion. Motivators are similar for Gen Z creators, however they are most motivated by ‘fun’, and more motivated by needing an outlet for anxiety. MOTIVATIONS FOR ENGAGING IN CREATIVE ACTIVITIES % Creators stated is current goal Creators Gen Z Creators 48% 48% 45% 43% 40% 40% 34% 32% 28% 29% 26% 26% 27% 24% 22% 20% 20% 19% 19% 15% Wanted to Looked fun Wanted Wanted Can make Had extra time Needed an Saw someone A social issue Friend / family express myself to explore an to challenge money/turn it on my hands outlet for my online posting or cause I care member interest or passion myself into a career during COVID stress / anxiety about it about recommended it Q3. What motivated you to start engaging in creative activities or creating original social media content? S16. Which of the following do you feel describes you? Base: Creators (n=4535), Gen Z Creators (n=5111) 24

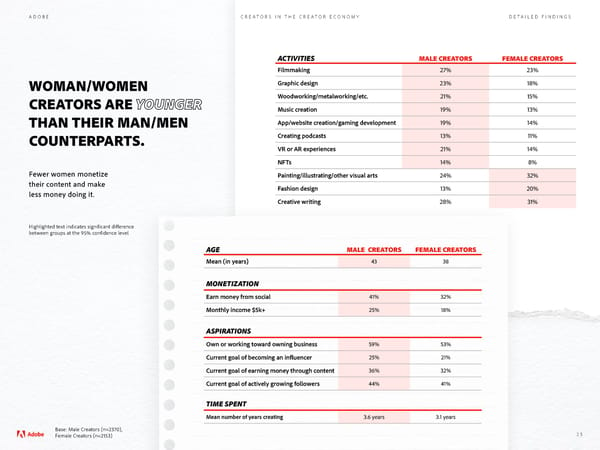

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS ACTIVITIES MALE CREATORS FEMALE CREATORS Filmmaking 27% 23% WOMAN/WOMEN Graphic design 23% 18% CREATORS ARE YOUNGER Woodworking/metalworking/etc. 21% 15% Music creation 19% 13% THAN THEIR MAN/MEN App/website creation/gaming development 19% 14% COUNTERPARTS. Creating podcasts 13% 11% VR or AR experiences 21% 14% NFTs 14% 8% Fewer women monetize Painting/illustrating/other visual arts 24% 32% their content and make Fashion design 13% 20% less money doing it. Creative writing 28% 31% Highlighted text indicates significant difference between groups at the 95% confidence level AGE MALE CREATORS FEMALE CREATORS Mean (in years) 43 38 MONETIZATION Earn money from social 41% 32% Monthly income $5k+ 25% 18% ASPIRATIONS Own or working toward owning business 59% 53% Current goal of becoming an in昀氀uencer 25% 21% Current goal of earning money through content 36% 32% Current goal of actively growing followers 44% 41% TIME SPENT Mean number of years creating 3.6 years 3.1 years Base: Male Creators (n=2370), Female Creators (n=2153) 25

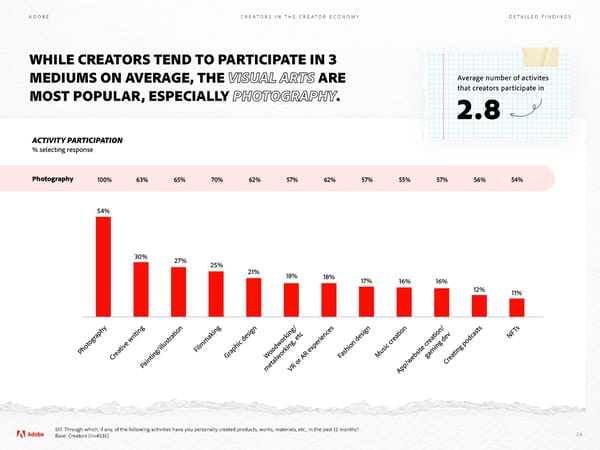

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS WHILE CREATORS TEND TO PARTICIPATE IN 3 MEDIUMS ON AVERAGE, THE VISUAL ARTS ARE Average number of activites MOST POPULAR, ESPECIALLY PHOTOGRAPHY. that creators participate in 2.8 ACTIVITY PARTICIPATION % selecting response Photography 100% 63% 65% 70% 62% 57% 62% 57% 55% 57% 56% 54% 54% 30% 27% 25% 21% 18% 18% 17% 16% 16% 12% 11% y g g gn g/ s gn ts Ts ritin tion in si kin tc si tion tion/ v as NF graph stra or , e ience ea ea odc to ve w u w g per g de ho ti ilmmak od kin x hion de sic cr te cr g p P ea g/ill F raphic de o or as u si amin tin Cr in G W w F M eb g ea aint tal Cr P me VR or AR e pp/w A S17. Through which, if any, of the following activities have you personally created products, works, materials, etc., in the past 12 months? Base: Creators (n=4535) 26

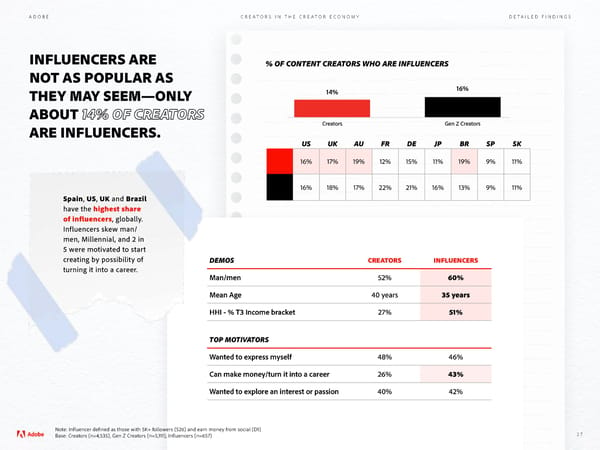

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS INFLUENCERS ARE % OF CONTENT CREATORS WHO ARE INFLUENCERS NOT AS POPULAR AS THEY MAY SEEM—ONLY 14% 16% ABOUT 14% OF CREATORS ARE INFLUENCERS. Creators Gen Z Creators US UK AU FR DE JP BR SP SK 16% 17% 19% 12% 15% 11% 19% 9% 11% 16% 18% 17% 22% 21% 16% 13% 9% 11% Spain, US, UK and Brazil have the highest share of influencers, globally. Influencers skew man/ men, Millennial, and 2 in 5 were motivated to start creating by possibility of DEMOS CREATORS INFLUENCERS turning it into a career. Man/men 52% 60% Mean Age 40 years 35 years HHI - % T3 Income bracket 27% 51% TOP MOTIVATORS Wanted to express myself 48% 46% Can make money/turn it into a career 26% 43% Wanted to explore an interest or passion 40% 42% Note: Influencer defined as those with 5K+ followers (S26) and earn money from social (D1) Base: Creators (n=4,535), Gen Z Creators (n=5,111), Influencers (n=657) 27

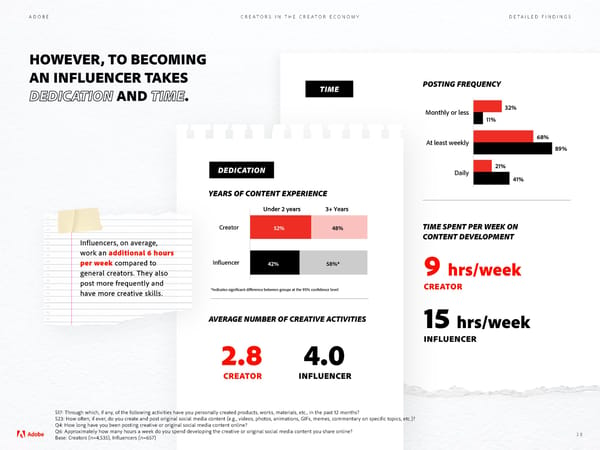

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS HOWEVER, TO BECOMING AN INFLUENCER TAKES POSTING FREQUENCY DEDICATION AND TIME. TIME Monthly or less 32% 11% At least weekly 68% 89% DEDICATION 21% Daily 41% YEARS OF CONTENT EXPERIENCE Under 2 years 3+ Years Creator 52% 48% TIME SPENT PER WEEK ON Influencers, on average, CONTENT DEVELOPMENT work an additional 6 hours per week compared to In uencer 42% 58%* general creators. They also 9 hrs/week post more frequently and CREATOR have more creative skills. *Indicates signi cant di erence between groups at the 95% con dence level AVERAGE NUMBER OF CREATIVE ACTIVITIES 15 hrs/week 2.8 4.0 INFLUENCER CREATOR INFLUENCER S17: Through which, if any, of the following activities have you personally created products, works, materials, etc., in the past 12 months? S23: How often, if ever, do you create and post original social media content (e.g., videos, photos, animations, GIFs, memes, commentary on specific topics, etc.)? Q4: How long have you been posting creative or original social media content online? Q6: Approximately how many hours a week do you spend developing the creative or original social media content you share online? 28 Base: Creators (n=4,535), Influencers (n=657)

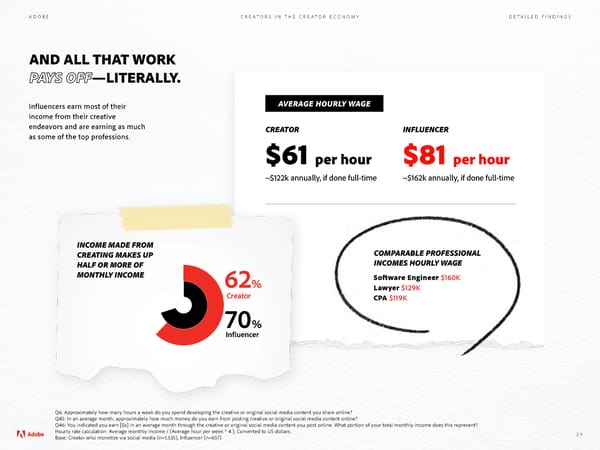

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS AND ALL THAT WORK PAYS OFF—LITERALLY. Influencers earn most of their AVERAGE HOURLY WAGE income from their creative endeavors and are earning as much CREATOR INFLUENCER as some of the top professions. $61 per hour $81 per hour ~$122k annually, if done full-time ~$162k annually, if done full-time INCOME MADE FROM CREATING MAKES UP COMPARABLE PROFESSIONAL HALF OR MORE OF INCOMES HOURLY WAGE MONTHLY INCOME 62% Software Engineer $160K Lawyer $129K Creator CPA $119K 70% In uencer Q6. Approximately how many hours a week do you spend developing the creative or original social media content you share online? Q45: In an average month, approximately how much money do you earn from posting creative or original social media content online? Q46: You indicated you earn [$x] in an average month through the creative or original social media content you post online. What portion of your total monthly income does this represent? Hourly rate calculation: Average monthly income / (Average hour per week * 4 ); Converted to US dollars. 29 Base: Creator who monetize via social media (n=1,535), Influencer (n=657)

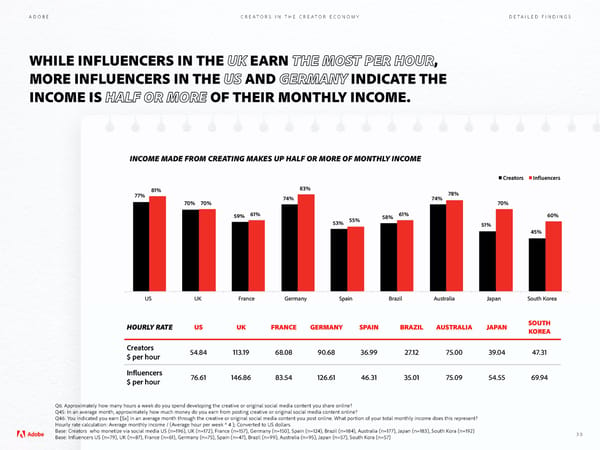

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS WHILE INFLUENCERS IN THE UK EARN THE MOST PER HOUR, MORE INFLUENCERS IN THE US AND GERMANY INDICATE THE INCOME IS HALF OR MORE OF THEIR MONTHLY INCOME. INCOME MADE FROM CREATING MAKES UP HALF OR MORE OF MONTHLY INCOME Creators In uencers 81% 83% 78% 77% 74% 74% 70% 70% 70% 59% 61% 58% 61% 60% 53% 55% 51% 45% US UK France Germany Spain Brazil Australia Japan South Korea HOURLY RATE US UK FRANCE GERMANY SPAIN BRAZIL AUSTRALIA JAPAN SOUTH KOREA Creators 54.84 113.19 68.08 90.68 36.99 27.12 75.00 39.04 47.31 $ per hour In昀氀uencers 76.61 146.86 83.54 126.61 46.31 35.01 75.09 54.55 69.94 $ per hour Q6. Approximately how many hours a week do you spend developing the creative or original social media content you share online? Q45: In an average month, approximately how much money do you earn from posting creative or original social media content online? Q46: You indicated you earn [$x] in an average month through the creative or original social media content you post online. What portion of your total monthly income does this represent? Hourly rate calculation: Average monthly income / (Average hour per week * 4 ); Converted to US dollars. Base: Creators who monetize via social media US (n=196), UK (n=172), France (n=157), Germany (n=150), Spain (n=124), Brazil (n=184), Australia (n=177), Japan (n=183), South Kora (n=192) 30 Base: Influencers US (n=79), UK (n=87), France (n=61), Germany (n=75), Spain (n=47), Brazil (n=99), Australia (n=95), Japan (n=57), South Kora (n=57)

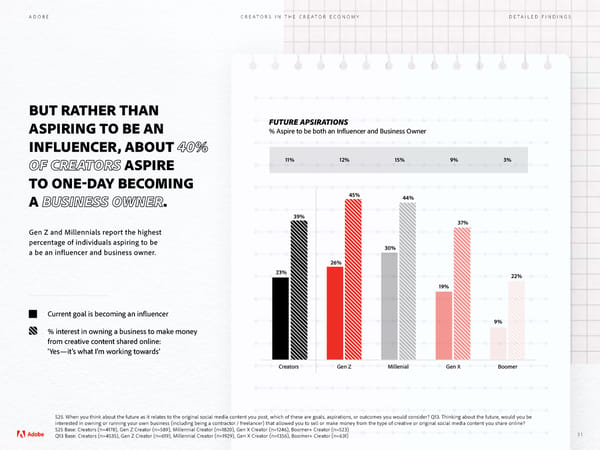

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS BUT RATHER THAN FUTURE APSIRATIONS ASPIRING TO BE AN % Aspire to be both an In昀氀uencer and Business Owner INFLUENCER, ABOUT 40% OF CREATORS ASPIRE 11% 12% 15% 9% 3% TO ONE-DAY BECOMING A BUSINESS OWNER. 45% 44% 39% 37% Gen Z and Millennials report the highest percentage of individuals aspiring to be 30% a be an influencer and business owner. 26% 23% 22% 19% Current goal is becoming an in昀氀uencer 9% % interest in owning a business to make money from creative content shared online: ‘Yes—it’s what I’m working towards’ Creators Gen Z Millenial Gen X Boomer S25. When you think about the future as it relates to the original social media content you post, which of these are goals, aspirations, or outcomes you would consider? Q13. Thinking about the future, would you be interested in owning or running your own business (including being a contractor / freelancer) that allowed you to sell or make money from the type of creative or original social media content you share online? S25 Base: Creators (n=4178), Gen Z Creator (n=589), Millennial Creator (n=1820), Gen X Creator (n=1246), Boomer+ Creator (n=523) Q13 Base: Creators (n=4535), Gen Z Creator (n=619), Millennial Creator (n=1929), Gen X Creator (n=1356), Boomer+ Creator (n=631) 31

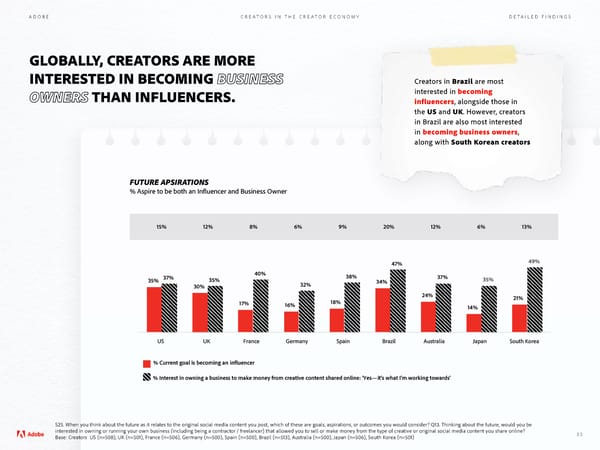

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS GLOBALLY, CREATORS ARE MORE INTERESTED IN BECOMING BUSINESS Creators in Brazil are most OWNERS THAN INFLUENCERS. interested in becoming influencers, alongside those in the US and UK. However, creators in Brazil are also most interested in becoming business owners, along with South Korean creators FUTURE APSIRATIONS % Aspire to be both an In昀氀uencer and Business Owner 15% 12% 8% 6% 9% 20% 12% 6% 13% 47% 49% 37% 40% 38% 37% 35% 35% 32% 34% 35% 30% 24% 21% 17% 16% 18% 14% US UK France Germany Spain Brazil Australia Japan South Korea % Current goal is becoming an in uencer % Interest in owning a business to make money from creative content shared online: ‘Yes—it’s what I’m working towards’ S25. When you think about the future as it relates to the original social media content you post, which of these are goals, aspirations, or outcomes you would consider? Q13. Thinking about the future, would you be interested in owning or running your own business (including being a contractor / freelancer) that allowed you to sell or make money from the type of creative or original social media content you share online? 32 Base: Creators US (n=508), UK (n=501), France (n=506), Germany (n=500), Spain (n=500), Brazil (n=513), Australia (n=500), Japan (n=506), South Korea (n=501)

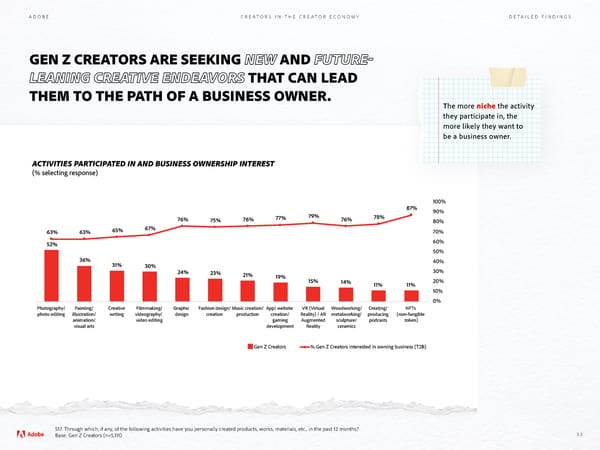

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS GEN Z CREATORS ARE SEEKING NEW AND FUTURE- LEANING CREATIVE ENDEAVORS THAT CAN LEAD THEM TO THE PATH OF A BUSINESS OWNER. The more niche the activity they participate in, the more likely they want to be a business owner. ACTIVITIES PARTICIPATED IN AND BUSINESS OWNERSHIP INTEREST (% selecting response) 100% 87% 90% 76% 75% 76% 77% 79% 76% 78% 80% 63% 63% 65% 67% 70% 52% 60% 50% 36% 31% 40% 30% 30% 24% 23% 21% 19% 15% 14% 11% 11% 20% 10% 0% Photography/ Painting/ Creative Filmmaking/ Graphic Fashion design/ Music creation/ App/ website VR (Virtual Woodworking/ Creating/ NFTs photo editing illustration/ writing videography/ design creation production creation/ Reality) / AR metalworking/ producing (non-fungible animation/ video editing gaming Augmented sculpture/ podcasts token) visual arts development Reality ceramics Gen Z Creators % Gen Z Creators interested in owning business (T2B) S17. Through which, if any, of the following activities have you personally created products, works, materials, etc., in the past 12 months? Base: Gen Z Creators (n=5,111) 33

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS CREATING ON SOCIAL IS ESSENTIAL FOR EMOTIONAL WELL-BEING 34

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS “Creative people are happy people.” — CREATOR, SOUTH KOREA 35

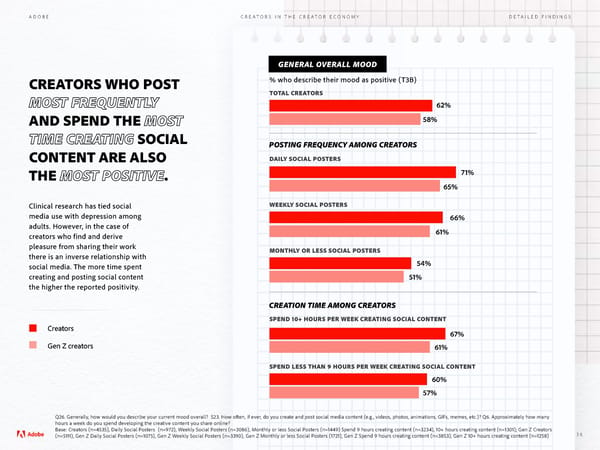

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS GENERAL OVERALL MOOD CREATORS WHO POST % who describe their mood as positive (T3B) MOST FREQUENTLY TOTAL CREATORS 62% AND SPEND THE MOST 58% TIME CREATING SOCIAL POSTING FREQUENCY AMONG CREATORS CONTENT ARE ALSO DAILY SOCIAL POSTERS THE MOST POSITIVE. 71% 65% Clinical research has tied social WEEKLY SOCIAL POSTERS media use with depression among 66% adults. However, in the case of 61% creators who find and derive pleasure from sharing their work MONTHLY OR LESS SOCIAL POSTERS there is an inverse relationship with 54% social media. The more time spent creating and posting social content 51% the higher the reported positivity. CREATION TIME AMONG CREATORS SPEND 10+ HOURS PER WEEK CREATING SOCIAL CONTENT Creators 67% Gen Z creators 61% SPEND LESS THAN 9 HOURS PER WEEK CREATING SOCIAL CONTENT 60% 57% Q26. Generally, how would you describe your current mood overall? S23. How often, if ever, do you create and post social media content (e.g., videos, photos, animations, GIFs, memes, etc.)? Q6. Approximately how many hours a week do you spend developing the creative content you share online? Base: Creators (n=4535), Daily Social Posters (n=972), Weekly Social Posters (n=3086), Monthly or less Social Posters (n=1449) Spend 9 hours creating content (n=3234), 10+ hours creating content (n=1301); Gen Z Creators (n=5111), Gen Z Daily Social Posters (n=1075), Gen Z Weekly Social Posters (n=3390), Gen Z Monthly or less Social Posters (1721), Gen Z Spend 9 hours creating content (n=3853), Gen Z 10+ hours creating content (n=1258) 36

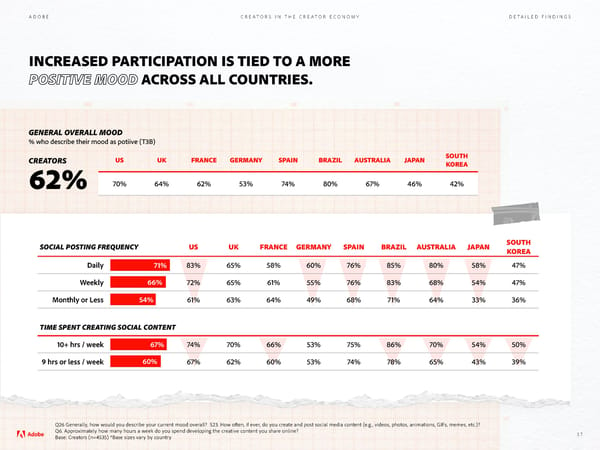

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS INCREASED PARTICIPATION IS TIED TO A MORE POSITIVE MOOD ACROSS ALL COUNTRIES. GENERAL OVERALL MOOD % who describe their mood as potiive (T3B) CREATORS US UK FRANCE GERMANY SPAIN BRAZIL AUSTRALIA JAPAN SOUTH KOREA 62% 70% 64% 62% 53% 74% 80% 67% 46% 42% SOCIAL POSTING FREQUENCY US UK FRANCE GERMANY SPAIN BRAZIL AUSTRALIA JAPAN SOUTH KOREA Daily 71% 83% 65% 58% 60% 76% 85% 80% 58% 47% Weekly 66% 72% 65% 61% 55% 76% 83% 68% 54% 47% Monthly or Less 54% 61% 63% 64% 49% 68% 71% 64% 33% 36% TIME SPENT CREATING SOCIAL CONTENT 10+ hrs / week 67% 74% 70% 66% 53% 75% 86% 70% 54% 50% 9 hrs or less / week 60% 67% 62% 60% 53% 74% 78% 65% 43% 39% Q26 Generally, how would you describe your current mood overall? S23. How often, if ever, do you create and post social media content (e.g., videos, photos, animations, GIFs, memes, etc.)? Q6. Approximately how many hours a week do you spend developing the creative content you share online? 37 Base: Creators (n=4535) *Base sizes vary by country

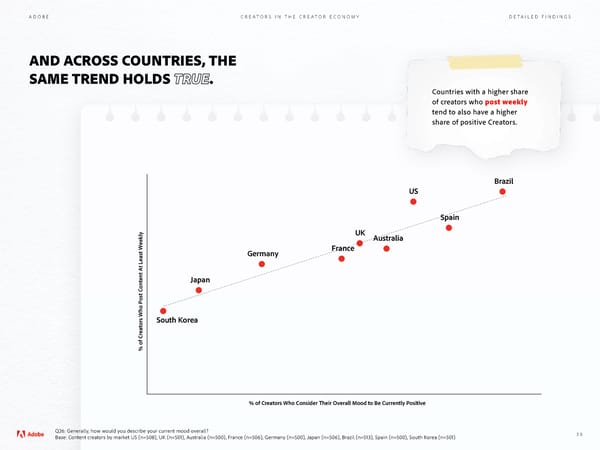

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS AND ACROSS COUNTRIES, THE SAME TREND HOLDS TRUE. Countries with a higher share of creators who post weekly tend to also have a higher share of positive Creators. Brazil US Spain UK Australia Germany France Japan South Korea % of Creators Who Post Content At Least Weekly % of Creators Who Consider eir Overall Mood to Be Currently Positive Q26: Generally, how would you describe your current mood overall? 38 Base: Content creators by market US (n=508), UK (n=501), Australia (n=500), France (n=506), Germany (n=500), Japan (n=506), Brazil (n=513), Spain (n=500), South Korea (n=501)

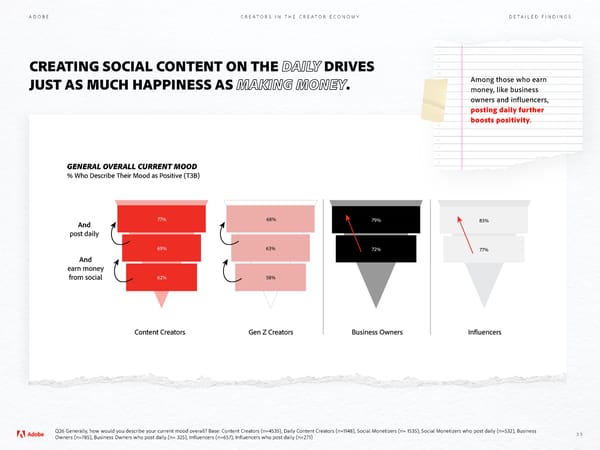

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS CREATING SOCIAL CONTENT ON THE DAILY DRIVES JUST AS MUCH HAPPINESS AS MAKING MONEY. Among those who earn money, like business owners and influencers, posting daily further boosts positivity. GENERAL OVERALL CURRENT MOOD % Who Describe 吀栀eir Mood as Positive (T3B) And 77% 68% 79% 83% post daily 69% 63% 72% 77% And earn money from social 62% 58% Content Creators Gen Z Creators Business Owners In uencers Q26 Generally, how would you describe your current mood overall? Base: Content Creators (n=4535), Daily Content Creators (n=1148), Social Monetizers (n= 1535), Social Monetizers who post daily (n=532), Business 39 Owners (n=785), Business Owners who post daily (n= 325), Influencers (n=657), Influencers who post daily (n=271)

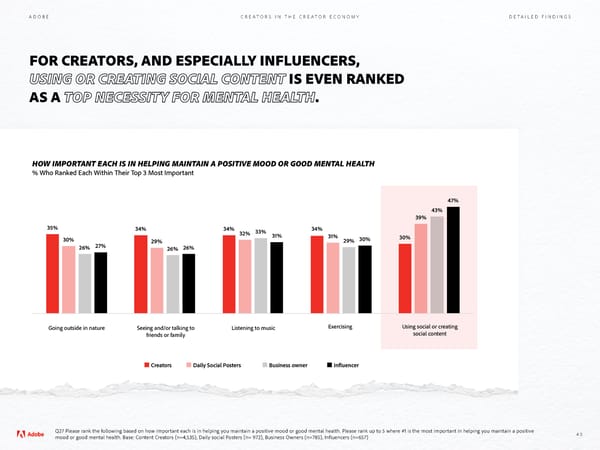

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS FOR CREATORS, AND ESPECIALLY INFLUENCERS, USING OR CREATING SOCIAL CONTENT IS EVEN RANKED AS A TOP NECESSITY FOR MENTAL HEALTH. HOW IMPORTANT EACH IS IN HELPING MAINTAIN A POSITIVE MOOD OR GOOD MENTAL HEALTH % Who Ranked Each Within 吀栀eir Top 3 Most Important 47% 43% 39% 35% 34% 34% 33% 34% 32% 31% 31% 30% 30% 29% 29% 30% 26% 27% 26% 26% ` Going outside in nature Seeing and/or talking to Listening to music Exercising Using social or creating friends or family social content Creators Daily Social Posters Business owner In uencer Q27 Please rank the following based on how important each is in helping you maintain a positive mood or good mental health. Please rank up to 5 where #1 is the most important in helping you maintain a positive 40 mood or good mental health. Base: Content Creators (n=4,535), Daily social Posters (n= 972), Business Owners (n=785), Influencers (n=657)

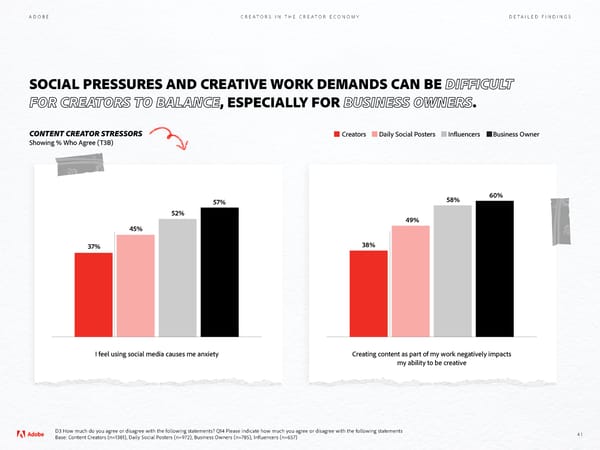

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS SOCIAL PRESSURES AND CREATIVE WORK DEMANDS CAN BE DIFFICULT FOR CREATORS TO BALANCE, ESPECIALLY FOR BUSINESS OWNERS. CONTENT CREATOR STRESSORS Creators Daily Social Posters In昀氀uencers Business Owner Showing % Who Agree (T3B) 58% 60% 57% 52% 49% 45% 37% 38% I feel using social media causes me anxiety Creating content as part of my work negatively impacts my ability to be creative D3 How much do you agree or disagree with the following statements? Q14 Please indicate how much you agree or disagree with the following statements 41 Base: Content Creators (n=1381), Daily Social Posters (n=972), Business Owners (n=785), Influencers (n=657)

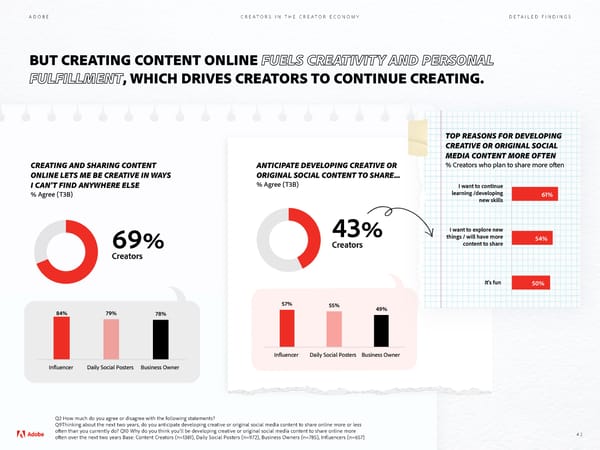

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS BUT CREATING CONTENT ONLINE FUELS CREATIVITY AND PERSONAL FULFILLMENT, WHICH DRIVES CREATORS TO CONTINUE CREATING. TOP REASONS FOR DEVELOPING CREATIVE OR ORIGINAL SOCIAL MEDIA CONTENT MORE OFTEN CREATING AND SHARING CONTENT ANTICIPATE DEVELOPING CREATIVE OR % Creators who plan to share more o昀琀en ONLINE LETS ME BE CREATIVE IN WAYS ORIGINAL SOCIAL CONTENT TO SHARE... I CAN’T FIND ANYWHERE ELSE % Agree (T3B) I want to continue % Agree (T3B) learning /developing 61% new skills 43 I want to explore new things / will have more 54% 69 Creators content to share Creators It’s fun 50% 57% 55% 49% 84% 79% 78% In uencer Daily Social Posters Business Owner In uencer Daily Social Posters Business Owner Q2 How much do you agree or disagree with the following statements? Q9Thinking about the next two years, do you anticipate developing creative or original social media content to share online more or less often than you currently do? Q10 Why do you think you’ll be developing creative or original social media content to share online more 42 often over the next two years Base: Content Creators (n=1381), Daily Social Posters (n=972), Business Owners (n=785), Influencers (n=657)

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS A CALL FOR SOCIAL CAUSE CREATORS 43

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS A CREATIVE PERSON IS... “ Trying everything and not being afraid of failure” — CREATOR, JAPAN 44

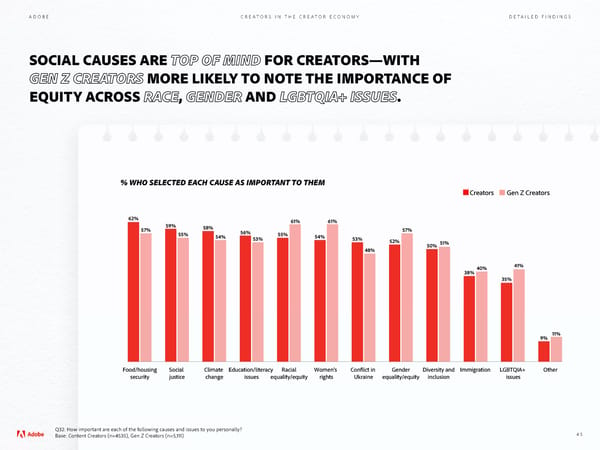

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS SOCIAL CAUSES ARE TOP OF MIND FOR CREATORS—WITH GEN Z CREATORS MORE LIKELY TO NOTE THE IMPORTANCE OF EQUITY ACROSS RACE, GENDER AND LGBTQIA+ ISSUES. % WHO SELECTED EACH CAUSE AS IMPORTANT TO THEM Creators Gen Z Creators 62% 61% 61% 57% 59% 58% 57% 55% 54% 56% 55% 54% 53% 53% 52% 51% 48% 50% 40% 41% 38% 35% 9% 11% Food/housing Social Climate Education/literacy Racial Women’s Con ict in Gender Diversity and Immigration LGBTQIA+ Other security justice change issues equality/equity rights Ukraine equality/equity inclusion issues Q32: How important are each of the following causes and issues to you personally? Base: Content Creators (n=4535), Gen Z Creators (n=5,111) 45

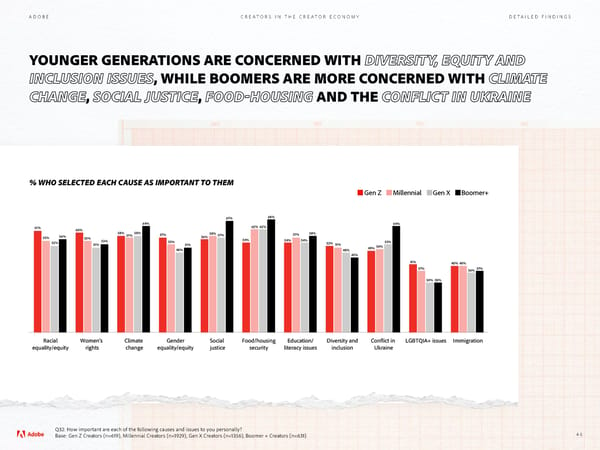

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS YOUNGER GENERATIONS ARE CONCERNED WITH DIVERSITY, EQUITY AND INCLUSION ISSUES, WHILE BOOMERS ARE MORE CONCERNED WITH CLIMATE CHANGE, SOCIAL JUSTICE, FOOD-HOUSING AND THE CONFLICT IN UKRAINE % WHO SELECTED EACH CAUSE AS IMPORTANT TO THEM Gen Z Millennial Gen X Boomer+ 67% 68% 64% 64% 61% 60% 62% 62% 58% 57% 58% 57% 58% 57% 57% 58% 55% 56% 55% 56% 52% 53% 53% 54% 54% 54% 53% 51% 51% 52% 51% 50% 48% 48% 49% 45% 41% 40 40% 37% 36% 37% 30% 30% Racial Women’s Climate Gender Social Food/housing Education/ Diversity and Con ict in LGBTQIA+ issues Immigration equality/equity rights change equality/equity justice security literacy issues inclusion Ukraine Q32: How important are each of the following causes and issues to you personally? Base: Gen Z Creators (n=619), Millennial Creators (n=1929), Gen X Creators (n=1356), Boomer + Creators (n=631) 46

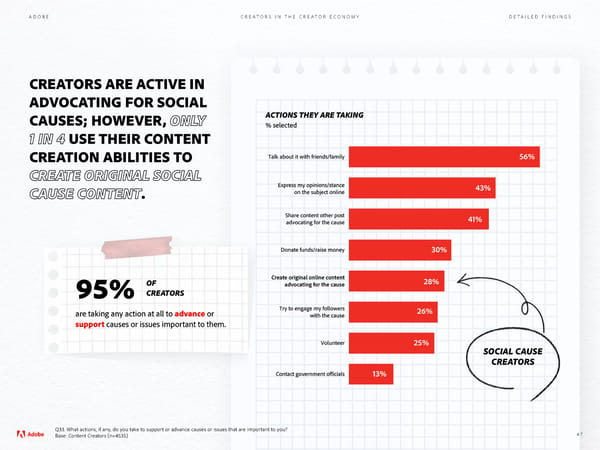

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS CREATORS ARE ACTIVE IN ADVOCATING FOR SOCIAL CAUSES; HOWEVER, ONLY ACTIONS THEY ARE TAKING % selected 1 IN 4 USE THEIR CONTENT CREATION ABILITIES TO Talk about it with friends/family 56% CREATE ORIGINAL SOCIAL Express my opinions/stance 43% CAUSE CONTENT. on the subject online Share content other post 41% advocating for the cause Donate funds/raise money 30% OF Create original online content 28% advocating for the cause 95% CREATORS are taking any action at all to advance or Try to engage my followers 26% with the cause support causes or issues important to them. Volunteer 25% SOCIAL CAUSE CREATORS Contact government o cials 13% Q33. What actions, if any, do you take to support or advance causes or issues that are important to you? Base: Content Creators (n=4535) 47

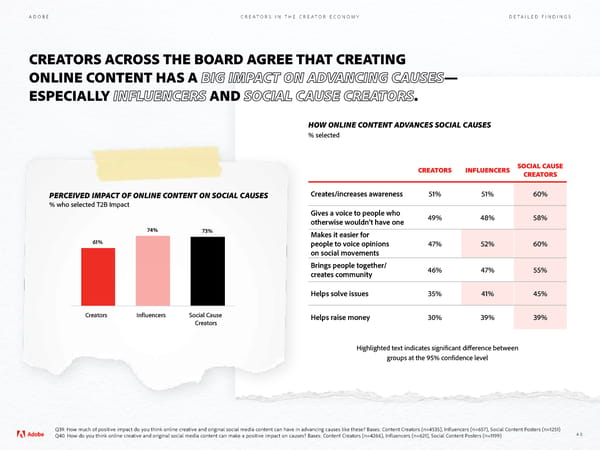

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS CREATORS ACROSS THE BOARD AGREE THAT CREATING ONLINE CONTENT HAS A BIG IMPACT ON ADVANCING CAUSES— ESPECIALLY INFLUENCERS AND SOCIAL CAUSE CREATORS. HOW ONLINE CONTENT ADVANCES SOCIAL CAUSES % selected CREATORS INFLUENCERS SOCIAL CAUSE CREATORS PERCEIVED IMPACT OF ONLINE CONTENT ON SOCIAL CAUSES Creates/increases awareness 51% 51% 60% % who selected T2B Impact Gives a voice to people who 49% 48% 58% otherwise wouldn’t have one 74% 73% Makes it easier for 61% people to voice opinions 47% 52% 60% on social movements Brings people together/ 46% 47% 55% creates community Helps solve issues 35% 41% 45% Creators In uencers Social Cause Helps raise money 30% 39% 39% Creators Highlighted text indicates signi昀椀cant di昀昀erence between groups at the 95% con昀椀dence level Q39. How much of positive impact do you think online creative and original social media content can have in advancing causes like these? Bases: Content Creators (n=4535), Influencers (n=657), Social Content Posters (n=1251) Q40. How do you think online creative and original social media content can make a positive impact on causes? Bases: Content Creators (n=4266), Influencers (n=621), Social Content Posters (n=1199) 48

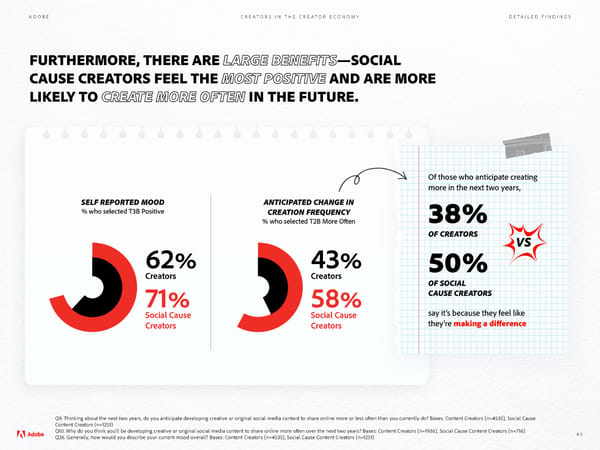

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS FURTHERMORE, THERE ARE LARGE BENEFITS—SOCIAL CAUSE CREATORS FEEL THE MOST POSITIVE AND ARE MORE LIKELY TO CREATE MORE OFTEN IN THE FUTURE. Of those who anticipate creating more in the next two years, SELF REPORTED MOOD ANTICIPATED CHANGE IN % who selected T3B Positive CREATION FREQUENCY 38% % who selected T2B More O昀琀en OF CREATORS VS 62 43 50% Creators Creators OF SOCIAL CAUSE CREATORS 71 58 Social Cause Social Cause say it’s because they feel like Creators Creators they’re making a di昀昀erence Q9. Thinking about the next two years, do you anticipate developing creative or original social media content to share online more or less often than you currently do? Bases: Content Creators (n=4535), Social Cause Content Creators (n=1251) Q10. Why do you think you’ll be developing creative or original social media content to share online more often over the next two years? Bases: Content Creators (n=1936), Social Cause Content Creators (n=716) 49 Q26. Generally, how would you describe your current mood overall? Bases: Content Creators (n=4535), Social Cause Content Creators (n=1251)

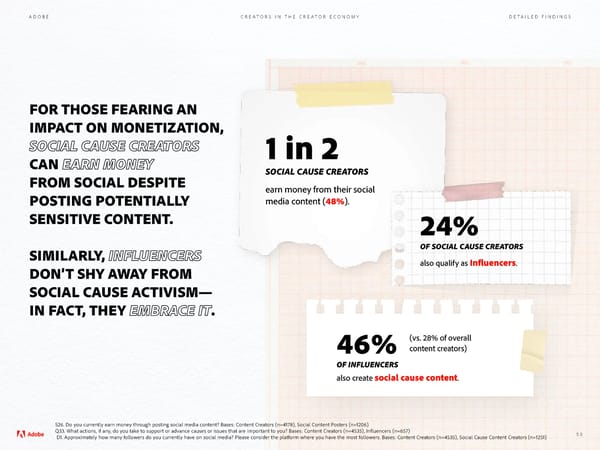

ADOBE CREATORS IN THE CREATOR ECONOMY DETAILED FINDINGS FOR THOSE FEARING AN IMPACT ON MONETIZATION, SOCIAL CAUSE CREATORS 1 in 2 CAN EARN MONEY SOCIAL CAUSE CREATORS FROM SOCIAL DESPITE earn money from their social POSTING POTENTIALLY media content (48%). SENSITIVE CONTENT. 24% SIMILARLY, INFLUENCERS OF SOCIAL CAUSE CREATORS DON’T SHY AWAY FROM also qualify as In昀氀uencers. SOCIAL CAUSE ACTIVISM— IN FACT, THEY EMBRACE IT. (vs. 28% of overall 46% content creators) OF INFLUENCERS social cause content. also create S26. Do you currently earn money through posting social media content? Bases: Content Creators (n=4178), Social Content Posters (n=1206) Q33. What actions, if any, do you take to support or advance causes or issues that are important to you? Bases: Content Creators (n=4535), Influencers (n=657) 50 D1. Approximately how many followers do you currently have on social media? Please consider the platform where you have the most followers. Bases: Content Creators (n=4535), Social Cause Content Creators (n=1251)

© 2022 Adobe. All rights reserved. Adobe, the Adobe logo, and the Document Cloud trefoil are either registered trademarks or trademarks of Adobe in the United States and/or other countries.